Despite infrastructure and manufacturing challenges that could

temper the pace of electric vehicle (EV) adoption, India's large

domestic automotive market, low existing EV penetration rates, and

increasing production capacity make it an attractive destination

for automakers and suppliers.

If Tata Motors' and Mahindra's success in navigating the

pandemic and semiconductor shortages is any indication, India is

expected to become a major player in global light vehicle

production. Furthermore, with global supply chain disruptions and

the return of protectionism, India's position as an export base for

mature markets is becoming increasingly viable.

Potential of India Automotive Industry to Bridge Gaps in Global

Supply Chain

Source: S&P Global Mobility Light

Vehicle Production Forecast

The Resilience of India Automotive Industry

While major markets like mainland China, the United States, and

Germany grappled with production setbacks during disruptions caused

by COVID-19 and semiconductor shortages, automotive industry in

India showed resilience. Indian automotive OEMs demonstrated a

stronger capability to secure semiconductor supplies despite having

lower purchasing power compared to global car manufacturers and

offering fewer features in their vehicles.

India's high GDP growth rate, which is further projected to

remain over 6% between 2026 and 2031, significantly higher than the

global average of 2.7%. India's domestic automotive market is a

significant draw for global automakers. As the 3rd largest market

in light vehicle sales and the 4th largest in light vehicle

production, India's low car penetration rate of just 38 vehicles

per 1,000 people presents a massive opportunity for the automotive

industry of India. According to

S&P Global Mobility Light Vehicle Production Forecasts,

production capacity is expected to rise from 6.8 million units in

2023 to 10 million by 2031, further solidifying India's role in the

global automotive landscape.

Concurrently, the US and EU's increased tariffs on Chinese EVs

have created a void that India is well-positioned to fill. With its

stable supply chain, light vehicle production growth in India is

expected to maintain a steady pace. S&P Global Mobility

projects a growth rate of 4 percent for 2024, with longer-term

expectations of growth stabilizing between 4% and 6% annually

through 2031.

A significant driver of this growth is the anticipated increase

in exports from major manufacturers like Maruti Suzuki and Hyundai,

which may benefit from the growing demand for affordable vehicles

in emerging markets.

Suzuki, for example, aims to ramp up production to 4 million

units by 2031, with a focus on hybrids and EVs.

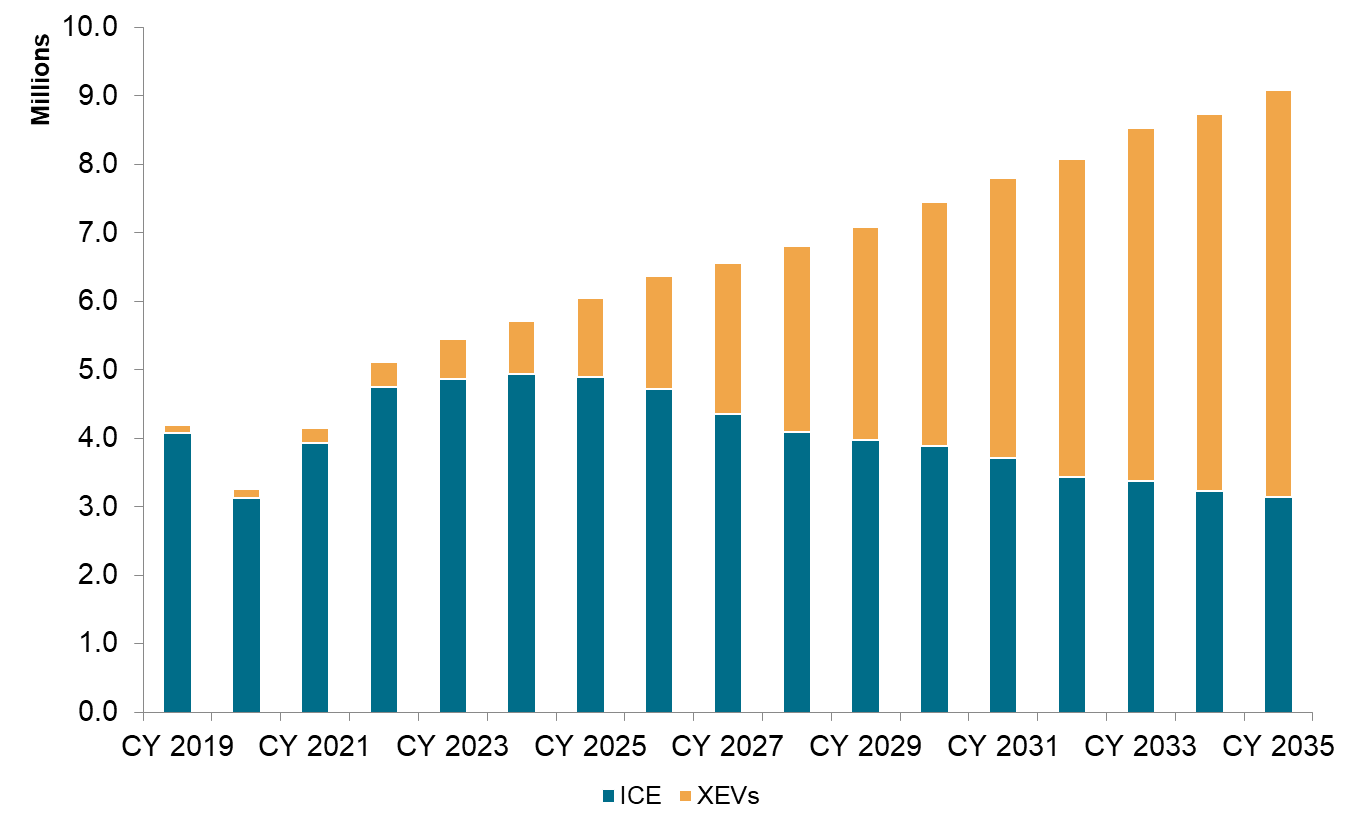

India Light Vehicle Production, xEV vs. ICE

{kind=link}

Data compiled: 8th July 2024.

Source: S&P Global Mobility.

XEVs = Mild Hybrid electric vehicle (MHEV)+ Hybrid

electric vehicle(HEV)+Plug in Hybrid vehicle (PHEV)+Range extender

electric vehicle (REX)+Battery Electric Vehicle (BEV)

Transition of India Automotive Industry to Clean

Technologies

India's automotive landscape is also shifting towards EVs. The

share of internal combustion engine (ICE) vehicles produced in

India is projected to decrease dramatically, from 97% in 2019 to

around 35% by 2035. The implementation of stricter emission

standards like the Bharat Stage 6 (BS6) and upcoming BS 7 norms

have pushed manufacturers to innovate and transition towards

cleaner technologies.

India automotive market is also witnessing a corresponding rise

in the adoption of low emission vehicles like xEVs. Demand for

hybrid electric vehicles (HEVs) and battery electric vehicles

(BEVs) is expected to grow substantially, with a notable increase

in hybrid, range extender vehicles and plug-in hybrid vehicles in

the short term.

However, the current state of infrastructure, particularly the

availability of charging stations and the overall EV ecosystem in

India automotive industry, could temper the pace of EV adoption.

Consumers and automakers are still somewhat cautious in the current

EV landscape. There is a noted delay in adopting new models and

platforms due to uncertainty surrounding regulatory conditions,

like the aforementioned BS7 emission norms.

High costs associated with early-stage EV manufacturing have

also led to rising vehicle prices, raising concerns about

affordability among first-time buyers. The increase in discounts

for ICE vehicles amid consumer trepidation and high inventory

levels could further slow the rate of adoption in the immediate

future.

Even with these mid-term pressures, the trend is unmistakable.

Vehicle manufacturers in India are increasingly adopting

multi-energy platforms that can support both internal combustion

engine (ICE) vehicles and EVs. Over the next few years, these

platforms are expected to increase in the market, setting the stage

for the eventual rise of dedicated EV platforms. Overall, the

long-term outlook for EVs in India is positive. As infrastructure

improves and consumer concerns are addressed, EV adoption is likely

to accelerate, according to S&P Global Mobility forecasts.

As India automotive industry is in the midst of a technological

revolution, there is also a heightened emphasis on supply chain

management. Innovations like ADAS (Advanced Driver Assistance

Systems), software-defined vehicles, and AI (Artificial

Intelligence) are becoming standard features, which require OEMs to

integrate these components into their supply chain.

This article is part of a series featuring highlights from

S&P Global Mobility's 2024 Solutions Webinar Series. The

webinar, India's Light Vehicle Production Outlook and Tata Motors'

Supply Chain Resiliance, occurred on July 16, 2024.

Watch the recording